IRS Formalizes Appeals Arbitration Process

In a prior posting, I highlighted a program entitled "Practical Dispute Resolution", that was scheduled for Thursday, October 19, 2006, which was National (& International) "Conflict Resolution Day".

One day before -- on Wednesday, October 18, 2006 -- the Internal Revenue Service, in its News Release IR-2006-163, found online here, announced permanent inclusion of a tested arbitration process within its standard tax appeals processes.

This is the text of the brief News Release:

Washington — The Internal Revenue Service announced today that the Appeals arbitration process is no longer a pilot program but part of business as usual at the IRS. In arbitration the IRS and the taxpayer agree to have a third party make a decision about a factual issue that will be binding on both of them.

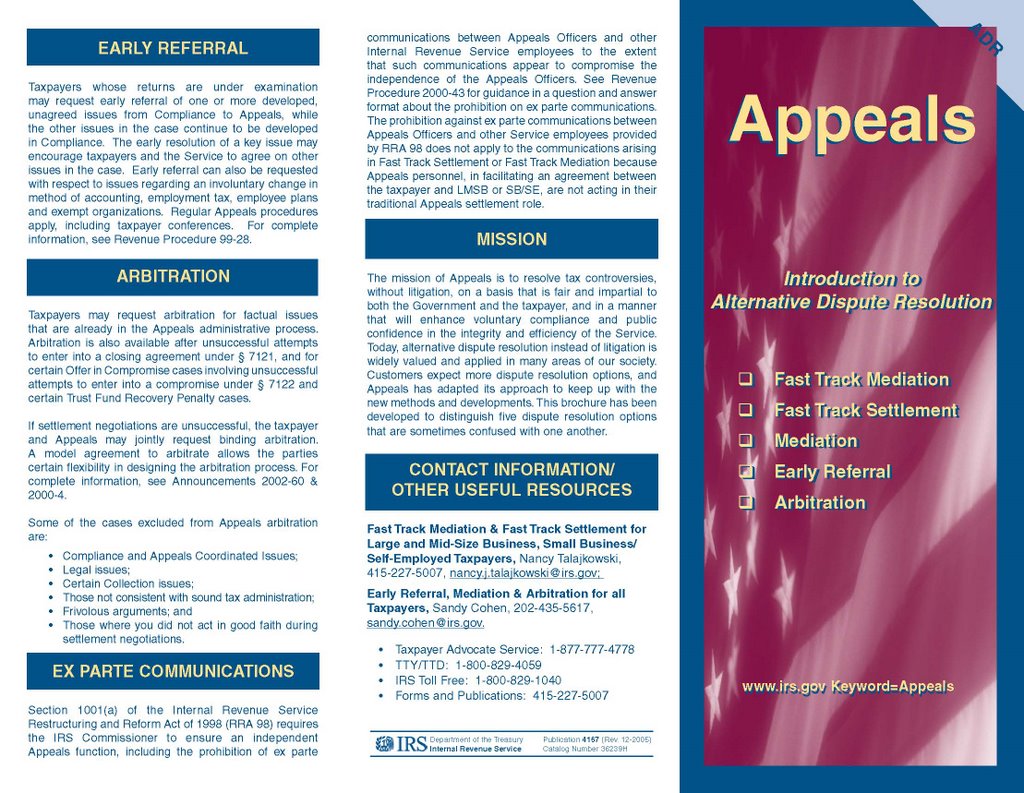

IRS Notice 2000-4 previously established a pilot program for cases in Appeals in which a taxpayer and IRS could jointly request binding arbitration on certain unresolved factual issues. When a limited number of factual issues remain unresolved during the course of an appeal, the taxpayer or the IRS can request arbitration and jointly select an Appeals or a non-IRS Arbitrator from any local or national organization that provides a roster of neutrals.

The permanent arbitration procedure may be used to resolve issues while a case is in Appeals, after settlement discussions are unsuccessful and, generally, when all other issues are resolved except specific factual issues for which arbitration is being requested.

Arbitration is not available for all issues. Some examples include legal issues, issues already in any court, issues in a taxpayer’s case designated for litigation, collection cases with certain exceptions, and frivolous issues.

The pilot program was created in 2000 for two years, then was extended, as follows:

- IRB 2000-3 -- Pursuant to section 7123(b)(2) of the Code, Appeals conducted a 2-year test of a binding arbitration procedure (Arbitration - Announcement 2000-4, 2000-3 IRB 317)

- Announcement 2000-4 -- Test of arbitration procedure for Appeals (Arbitration - Announcement 2002-60, 2002-26 IRB 28) -- This announcement extended the test of the arbitration procedures set forth in Announcement 2000-4, 2000-1 C.B. 317, for an additional one-year period.

- Appeals mediation procedure (Mediation - Rev. Proc.2002-44, 2002-26 IRB 10) -- This document formally established the Appeals mediation procedure, and modified and expanded the availability of mediation for cases that were already in the Appeals administrative process.

The "Alternative Dispute Resolution" web page of the IRS is found online here.